All Categories

Featured

Table of Contents

It's vital to note that your money is not directly bought the stock exchange. You can take money from your IUL anytime, however fees and surrender fees might be linked with doing so. If you need to access the funds in your IUL policy, considering the pros and disadvantages of a withdrawal or a car loan is vital.

Unlike straight financial investments in the stock market, your money value is not directly bought the underlying index. Rather, the insurance policy company makes use of economic tools like choices to link your cash money worth development to the index's performance. Among the unique attributes of IUL is the cap and floor prices.

What should I know before getting Iul Cash Value?

Upon the policyholder's death, the recipients get the fatality advantage, which is generally tax-free. The fatality advantage can be a set amount or can include the cash money value, depending on the policy's structure. The cash value in an IUL plan expands on a tax-deferred basis. This implies you don't pay taxes on the after-tax capital gains as long as the money continues to be in the plan.

Constantly review the plan's details and seek advice from an insurance coverage specialist to fully recognize the benefits, limitations, and expenses. An Indexed Universal Life Insurance coverage policy (IUL) supplies a distinct mix of attributes that can make it an eye-catching alternative for particular individuals. Below are several of the essential advantages:: Among one of the most attractive elements of IUL is the capacity for higher returns contrasted to various other kinds of permanent life insurance policy.

Iul

Withdrawing or taking a finance from your policy may minimize its cash money value, survivor benefit, and have tax implications.: For those curious about tradition planning, IUL can be structured to give a tax-efficient means to pass wide range to the following generation. The survivor benefit can cover estate taxes, and the cash worth can be an additional inheritance.

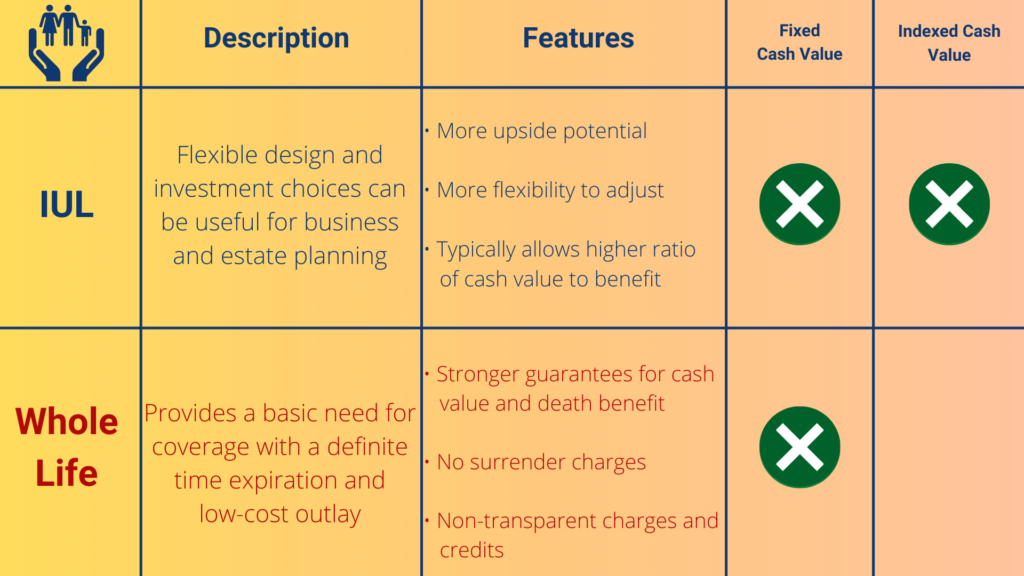

While Indexed Universal Life Insurance Policy (IUL) offers a series of benefits, it's important to think about the possible disadvantages to make a notified decision. Here are several of the crucial drawbacks: IUL plans are more intricate than standard term life insurance policy plans or entire life insurance policies. Comprehending how the money value is connected to a stock market index and the ramifications of cap and floor prices can be challenging for the average consumer.

The premiums cover not only the expense of the insurance however likewise administrative fees and the investment element, making it a pricier choice. IUL loan options. While the cash worth has the capacity for growth based upon a securities market index, that growth is frequently topped. If the index executes incredibly well in a given year, your gains will be restricted to the cap rate specified in your policy

: Adding optional features or cyclists can boost the cost.: Just how the policy is structured, including exactly how the cash money value is alloted, can additionally impact the cost.: Different insurance provider have different pricing versions, so looking around is wise.: These are charges for managing the plan and are generally deducted from the money worth.

Iul For Wealth Building

: The prices can be similar, however IUL uses a flooring to help safeguard against market recessions, which variable life insurance coverage policies normally do not. It isn't very easy to provide a precise cost without a certain quote, as prices can differ significantly between insurance coverage providers and individual circumstances. It's important to balance the importance of life insurance policy and the requirement for included defense it offers with possibly higher premiums.

They can help you understand the expenses and whether an IUL plan straightens with your financial goals and demands. Whether Indexed Universal Life Insurance Coverage (IUL) is "worth it" is subjective and depends on your economic objectives, risk resistance, and long-term planning demands. Below are some factors to consider:: If you're seeking a lasting financial investment vehicle that offers a survivor benefit, IUL can be a good option.

1 Your policy's money worth have to suffice to cover your month-to-month charges - IUL protection plan. Indexed global life insurance policy as utilized here describes policies that have actually not been signed up with U.S Securities and Exchange Payment. 2 Under current federal tax guidelines, you may access your cash money abandonment value by taking federal income tax-free financings or withdrawals from a life insurance policy policy that is not a Modified Endowment Contract (MEC) of approximately your basis (total costs paid) in the plan

How can Indexed Universal Life Cash Value protect my family?

If the plan lapses, is surrendered or comes to be a MEC, the finance equilibrium at the time would normally be considered as a circulation and as a result taxed under the general regulations for distribution of plan money values. This is a very general summary of the BrightLife Grow item. For expenses and even more total details, please contact your financial professional.

While IUL insurance might show useful to some, it's crucial to recognize how it works prior to purchasing a plan. Indexed universal life (IUL) insurance policies provide better upside prospective, adaptability, and tax-free gains.

What happens if I don’t have Iul Insurance?

business by market capitalization. As the index goes up or down, so does the rate of return on the cash worth part of your policy. The insurer that issues the plan may offer a minimum surefire price of return. There may likewise be an upper restriction or rate cap on returns.

Economists typically suggest living insurance policy protection that's comparable to 10 to 15 times your yearly earnings. There are a number of disadvantages connected with IUL insurance coverage that doubters fast to explain. For circumstances, somebody who establishes the plan over a time when the market is performing badly can wind up with high premium repayments that do not add in all to the cash value. Tax-advantaged IUL.

In addition to that, remember the following other factors to consider: Insurance policy firms can set participation prices for just how much of the index return you get annually. Let's state the plan has a 70% participation rate. If the index grows by 10%, your cash money worth return would be only 7% (10% x 70%).

Iul Plans

On top of that, returns on equity indexes are commonly capped at a maximum amount. A plan might claim your maximum return is 10% annually, despite how well the index does. These constraints can restrict the real rate of return that's credited towards your account every year, regardless of how well the policy's hidden index does.

IUL policies, on the various other hand, offer returns based on an index and have variable costs over time.

{kind=link}

Latest Posts

Who offers flexible Iul Cash Value plans?

Indexed Universal Life Tax Benefits

How long does Iul Premium Options coverage last?